They grow up so fast. At first it’s all about baby steps: a little bit of Apple to chew on, some Disney to watch, maybe even some Starbucks (for yourself) after they keep you up all night. As they gain confidence you let them dress themselves, no matter how silly their Small-Cap might look. You watch with pride as their Growth and Development starts paying Dividends. But now your IRA has entered its troublesome “RMD stage” and left you with an ever growing terror that your once charming retirement fund will break your happiness, your peace of mind, and most importantly your tax brackets. What do you do?

They grow up so fast. At first it’s all about baby steps: a little bit of Apple to chew on, some Disney to watch, maybe even some Starbucks (for yourself) after they keep you up all night. As they gain confidence you let them dress themselves, no matter how silly their Small-Cap might look. You watch with pride as their Growth and Development starts paying Dividends. But now your IRA has entered its troublesome “RMD stage” and left you with an ever growing terror that your once charming retirement fund will break your happiness, your peace of mind, and most importantly your tax brackets. What do you do?

First of all, don’t panic. This is a natural part of the IRA aging process. Once you reach 70 ½, any of your tax-deferred retirement accounts have to start paying out money called “required minimum distributions” (RMDs). These mandatory withdrawals have a reputation for causing headaches because you can’t control when they happen or how much (tax) damage they might cause. Your account starts acting like a teenager, only it’s more likely to own part of Facebook than log into it. And just like a teenager, it has energy that needs to be channeled. The key is patience and planning.

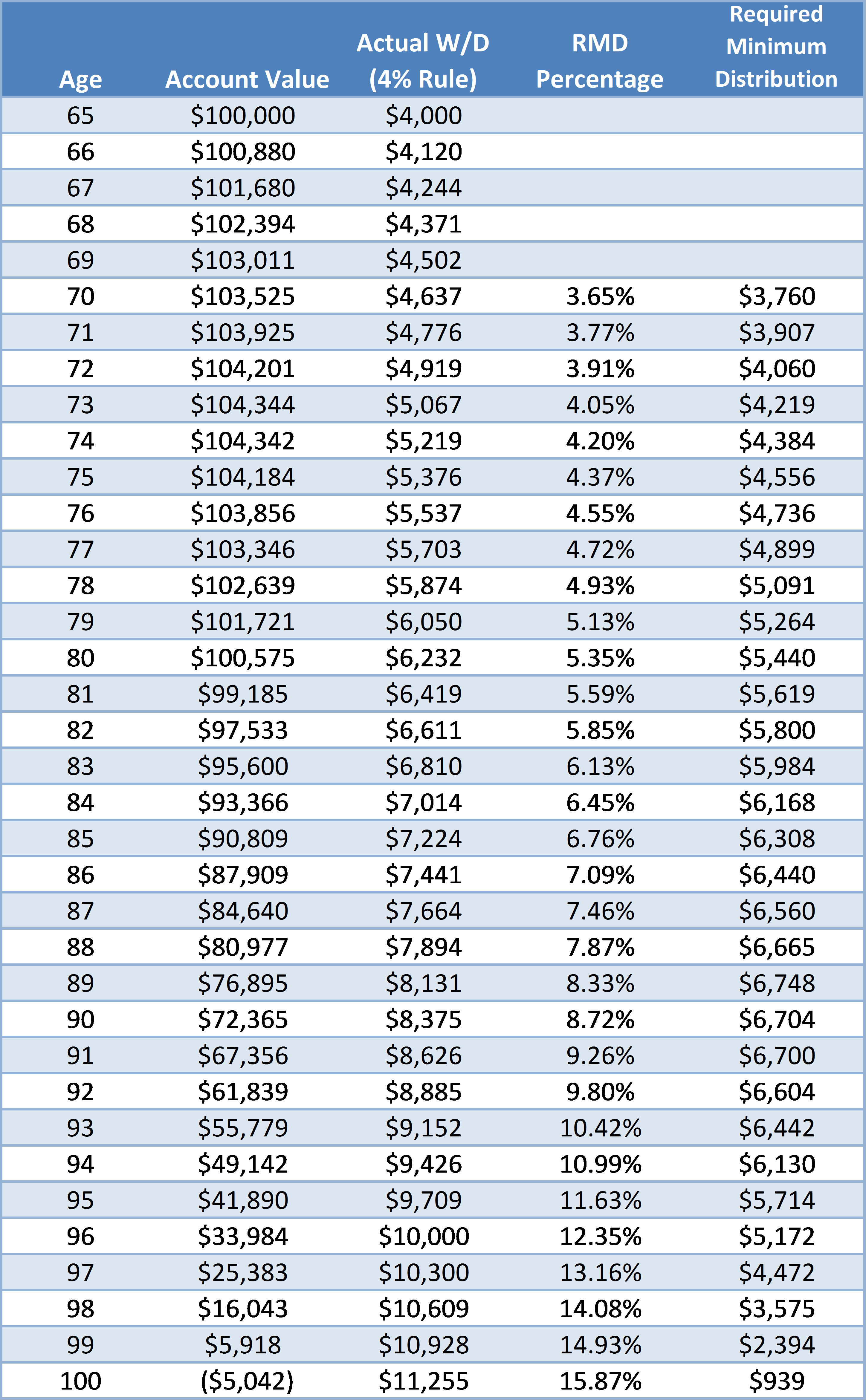

The good news is that for most, RMDs are manageable. The first required distribution at age 70 is about three and a half percent. If a hypothetical retiree starts taking money from their account using the four-percent rule at age 65 (assuming 5% annual returns and 3% inflation), the amount they withdraw every year will always be greater than their RMDs. What this boils down to is the average person is likely to run out of money on their own (in this case at age 99), without having to worry about a “required” distribution.

But not everyone falls into this category. Many retirees have a pension or spend frugally. Others keep working well into their seventies. And some lucky few benefit from unusually high investment returns, ending up with a huge IRA. Regardless, the story is the same: they are being forced by the IRS to withdraw more than they need, potentially hitting them with a substantial tax burden. Planning ahead is important in scenarios like these. Roth conversions can be used to “prepay” taxes, especially if done in lower brackets. Decreasing contributions to tax-deferred accounts in the immediate years before retirement can also help. But let’s state the obvious: this is a fortunate problem to have. If you don’t need to withdraw from your IRA or 401k for living expenses in retirement you should have little fear of “outlasting” your money.

By themselves RMDs are unlikely to impoverish a retiree, but keeping all the retirement eggs in a tax-deferred basket is still less than ideal. Long life expectancy (or an unexpectedly long life) combined with poor market returns can make budgeting more difficult because the percent that must be withdrawn goes up year after year. Estate planning is also challenging because the retiree must take distributions.

So although an RMD is generally not a threat to financial solvency, it is a threat to financial freedom. There are a wide variety of tools, from Roth IRAs to annuities to brokerage accounts, which can help groom any rambunctious tax-deferred wild child. Given time, planning, and a little love they can become a well-adjusted part of anyone’s golden years. Unless they’re actually in high-school. Then the advisors at Winch Financial make no promises.